DIFC Category 3A Brokerage License

Article Summary

- Matched Principal dealing has moved from Category 3A to Category 2, while Dealing in Investments as Agent remains a Category 3A activity with a reduced Base Capital requirement of US$ 200,000. Category 3A firms continue to fall under the DFSA’s Expense-Based Capital Minimum (EBCM) framework, generally set at 13/52 of annual audited expenditure, which maintains financial resilience for firms operating purely on an agency basis.

- DIFC is a top-10 global financial centre, offering an independent common-law court system, robust regulation, attractive tax efficiencies and full foreign ownership. It hosts over 400 wealth and asset managers with more than US$ 750 billion in assets, alongside 70+ hedge funds and over 850 family-owned businesses. This ecosystem, supported by a fast-growing HNWI population, makes the DIFC a natural hub for brokerage, trading and advisory platforms.

- Brokerage licensing spans across three categories, depending on the level of execution responsibility and risk assumed by the firm. Category 4 (Arranging Deals / Introducing Broker) involves no execution or custody, carries a Base Capital of around US$ 30,000, and suits referral or distribution-based models. Category 3A (Dealing as Agent) allows firms to execute trades strictly on behalf of clients without taking principal risk, and carries a Base Capital requirement of US$ 200,000. Category 2 covers higher-risk activities, including Matched Principal dealing with a Base Capital of US$ 500,000, and full Principal/Proprietary dealing with a Base Capital of US$ 2 million, combined with heightened governance and systems expectations.

- DIFC firms may service clients across the UAE provided that the regulated activity is conducted “in or from” the DIFC. However, the marketing of funds or onshore financial products may require compliance with additional SCA rules. DFSA-licensed brokers may also deal in Crypto Assets, provided these tokens are on the DFSA’s recognised list, which currently includes BTC, ETH, LTC, TON, XRP, ZETA, EURC, USDC and RLUSD, subject to appropriate controls and custody arrangements.

- Capital requirements are calculated as the highest of Base Capital, Risk-Based Capital and EBCM, and are dependent on the business model and financial projections. Firms must also appoint key individuals such as an SEO, FO, Risk Officer, CO/MLRO, and maintain a competent Board with non-executive oversight, alongside external and internal auditors. Setup costs typically include DFSA fees (around US$ 25,000 for a Category 3A application, plus per-activity charges), DIFC ROC fees for incorporation and licensing, data protection fees, office leasing within the DIFC, and visa/PSA expenses.

- The licensing process includes introductory meetings with the DIFC and DFSA, preparation of a detailed Regulatory Business Plan and financial model, submission of a comprehensive application pack (covering governance, AML, compliance, IT/cybersecurity, risk frameworks and KYC documentation), DFSA reviews and interviews, issuance of an In-Principle Approval, entity incorporation, capital funding and PI cover, followed by final DFSA approval. 10 Leaves provides end-to-end support across every stage, including document preparation, outsourced CO/MLRO/FO/Risk roles, corporate structuring, drafting of commercial and shareholder documents, and ongoing compliance, tax and secretarial services.

November 2025

Updates

There have been several key regulatory and operational developments in 2025 that directly affect Category 3A brokerage firms operating in the DIFC. The DFSA has updated prudential classifications and capital requirements, including a major structural change: Matched Principal dealing has now moved from Category 3A to Category 2, while Dealing in Investments as Agent remains a Category 3A activity with a revised Base Capital Requirement of US$ 200,000 (down from US$ 500,000 previously).

Category 3A firms are still subject to the DFSA’s Expense-Based Capital Minimum (EBCM) framework, which typically requires firms to maintain capital equal to 13/52 of annual audited expenditure, unless the DFSA determines a higher level of capital is necessary based on the firm’s risk profile. This approach emphasises operational resilience for agency brokerage models that do not hold client assets or take principal risk.

DIFC is one of the world’s top ten onshore financial centers and offers a secure and efficient platform for businesses and financial institutions to reach into and out of the emerging markets of the region. The quality and independence of DIFC’s regulator, the prevailing common law framework, excellent infrastructure and tax efficiencies make it the perfect base to take advantage of the rapidly growing demand for financial and business services in the MENASA region.

DIFC fills the time-zone gap for a global financial centre between the leading financial centres of London and New York in the West and Hong Kong and Tokyo in the East.

Why should you set up a financial services entity in the DIFC?

The DIFC stands as a premier financial center in the region, hosting over 400 wealth and asset management firms that collectively manage more than $750 billion in assets. This strategic location provides unparalleled access to the extensive private and sovereign capital available in the region.

The DIFC also offers an advanced regulatory framework for digital assets, encompassing investment and crypto tokens. It also features a dedicated Innovation Hub, supporting companies in the fintech, AI, and blockchain sectors.

Recently, there has been a notable and continuous influx of High-Net-Worth Individuals (HNIs) into the UAE. Dubai alone is home to over 72,500 HNWIs and Ultra-High-Net-Worth Individuals (UHNWIs), whose combined wealth exceeds $500 billion. The broader Middle Eastern region boasts over $3.5 trillion in HNWIs wealth and more than $4.8 trillion in financial capital managed by 40 state-owned investors.

The DIFC is witnessing high growth in the alternatives segment. It currently includes 70+ hedge funds, with over 45 of these managing over a billion dollars worldwide. As a result, the DIFC has emerged as one of the world's top ten locations for hedge funds, with ambitions to enter the top five in the near future.

The DIFC has been consistent in attracting family businesses as well, with over 850 family-owned businesses located in the centre, a growth of over 30% in 2024.

By the end of 2024, DIFC reported that the top 120 families and wealthy individuals in the community were managing over USD 1.2 trillion in wealth. The use of Foundations and associated structures also saw a 50+ percentage jump, reaching nearly 700 foundations by the end of 2024.

The Centre in the UAE is a cultural hub, featuring fine dining, retailers, and art galleries. Events like DIFC Art Nights and the Sculpture Park attract artists and enthusiasts. Art Dubai, backed by DIFC, remains the foremost global art event in the Middle East.

Specific Advantages

Here are some specific advantages of establishing in the Dubai International Financial Centre.

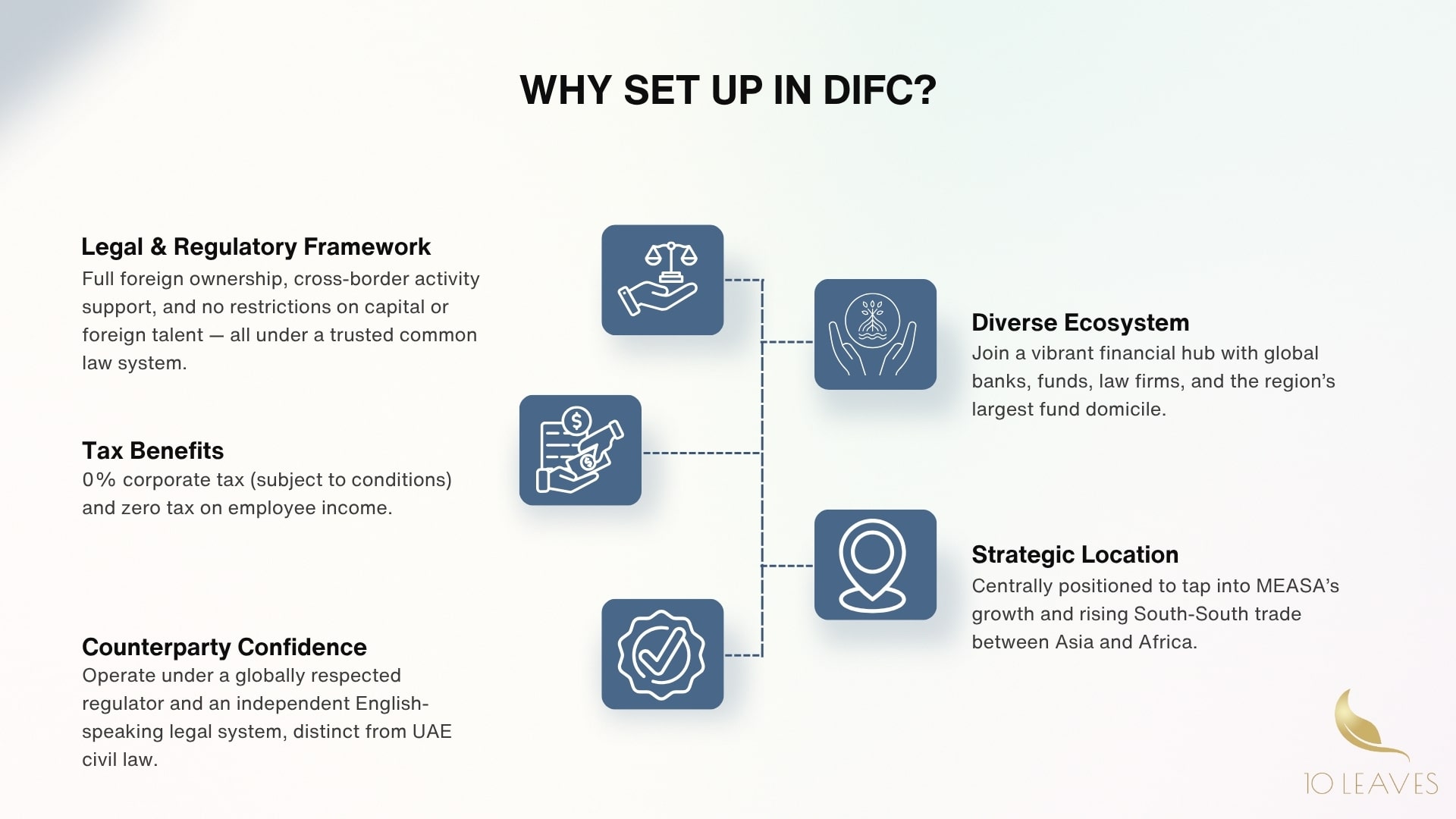

LEGAL AND REGULATORY FRAMEWORK

- Legal framework supports cross-border activities.

- 100% foreign ownership permitted.

- No restriction on foreign talent or employees.

- No restrictions on capital repatriation.

TAX BENEFITS

- 0 percent corporate tax subject to certain qualifications.

- Zero tax on employee income.

COUNTERPARTY CONFIDENCE

- Highly regarded, independent regulator.

- Independent, English-speaking, common law judicial system.

- Distinct from the UAE legal system.

- Risk-based regulatory approach.

DIVERSE ECOSYSTEM

- Central to regional deal making.

- High concentration of international firms, investment funds, wealth management firms, banks, and financial institutions.

- World-class regional and international law and auditing firms, and other professional services.

- The largest fund domicile in the region.

GEOGRAPHIC EPICENTRE

- Management offices, holding companies and family offices are located closer to the assets they own or manage.

- The Middle East, Africa and South Asia (MEASA) is increasingly the centre of gravity for the global economy.

- Dubai plays a central role in the growing South-South trade, principally between Asia and Africa.

- Well-positioned to harness the potential of emerging markets.

What kind of brokerage licenses are available in the DIFC?

Brokerage licensing is categorized by the level of risk the firm assumes, primarily distinguishing between acting as an agent, a matched principal, or a full principal. Firms wishing to execute trades on behalf of clients typically apply for the principal activity of ‘Dealing in Investments as Agent’, which falls in the Category 3A license classification, with a Base Capital of US$ 500,000.

Under this category, a broker can operate as an Agent, where they simply execute orders in the client's name without taking the other side of the trade, or as a Matched Principal. In the matched principal model (often called "riskless principal"), the broker interposes itself between the buyer and seller, entering into a transaction with the client and a simultaneous, matching transaction with a counterparty. While the broker is technically a principal to the trade, they do not hold "open" market positions or expose their own capital to market fluctuations. As per a recent DFSA update, matched principal activities now fall under Category 2, but keeping the Base Capital at US$ 500,000.

Conversely, acting as a Full Principal involves proprietary trading or market making where the firm holds inventory and assumes direct market risk; this higher-risk activity of ‘Dealing in Investments as Principal’ requires a Category 2 license and a significantly higher Base Capital of US$ 2 million.

Distinct from these execution-focused models is the Introducing Broker (IB) activity, which in the DIFC regulatory framework generally falls under ‘Arranging Deals in Investments’ - a Category 4 activity. An entity licensed for this activity does not execute trades or hold client assets. Instead, it focuses on marketing services and referring clients to other fully licensed brokers or financial institutions who handle the actual execution and custody. Because the Introducing Broker acts solely as an intermediary without touching client funds or entering the trade chain, the regulatory barrier to entry is lower, with Base Capital requirements at US$ 30,000, and no expense-based capital requirements. This makes it a common starting point for firms focusing on sales and relationship management rather than trade execution infrastructure. A point to note is that the DFSA does not encourage regulatory arbitrage, and hence license holders in non-DFSA recognised jurisdictions (typically the Caribbean, Labuan and New Zealand) may not be able to establish as Introducing Brokers to onboard clients and further service them offshore.

What does the DFSA consider as a Matched Principal activity?

A firm is considered to be operating on a Matched Principal basis when it deals as principal solely for the purpose of executing client orders, rather than taking proprietary positions. Any positions it holds arise only because a client order is temporarily unmatched, and these exposures must remain strictly limited — the market value of such positions cannot exceed 15% of the firm’s Tier 1 Capital. These positions are incidental and provisional in nature, existing only for the short period necessary to complete the back-to-back transaction.

Clients do not have a direct relationship with the Prime Broker. The firm acts as principal for execution but allocates internally.

Key Comparisons (Agent vs. Matched Principal)

|

Feature |

Matched Principal |

Dealing as Agent |

|

Balance Sheet Impact |

Yes |

No |

|

Client dealing with Prime Broker |

No |

No |

|

Trade Risk |

Yes (short-term) |

No |

|

Licensed Activity |

Dealing as Principal (Cat 2) |

Dealing as Agent (Cat 3A) |

|

Base Capital Requirement |

US$ 500,000 |

US$ 200,000 |

|

Revenue model |

Spread/Commission |

Commission only |

DIFC Regulated Brokerage Activities

Dealing in Investments as Agent

Dealing in Investments as Agent refers to a financial service activity where a firm executes investment transactions strictly on behalf of its clients, rather than for its own account. In this role, the firm acts as an intermediary between buyers and sellers, arranging and carrying out trades according to client instructions while never taking ownership of the investment itself.

Because the firm does not assume market risk, all positions and exposures arising from a transaction belong entirely to the client. The firm must ensure that each order is executed on the best available terms, maintain clear segregation of client assets, and implement systems that prevent conflicts of interest.

Under DFSA rules, this activity includes receiving and transmitting orders, negotiating trades for clients, and interacting with market counterparties as an agent. Importantly, the firm must not engage in matched principal or principal trading unless separately authorised. Dealing as Agent therefore remains a pure agency activity focused on representing client interests, facilitating execution, and ensuring transparent, compliant interaction with the market.

Dealing in Investments as Principal (Matched Principal basis only)

Dealing in Investments as Matched Principal is a financial service where a firm executes client orders by interposing itself between the buyer and seller, becoming principal to both sides of the transaction, but only on a matched, risk-neutral basis. The firm does not take proprietary positions for its own account; instead, any exposure arises solely because the client orders are not perfectly synchronised.

Under DFSA rules, a firm is considered a Matched Principal dealer when trading as principal strictly to fulfil client instructions and when any resulting positions are incidental, short-lived, and limited to the time required to complete the trade.

The firm must ensure that the market value of any such temporary positions does not exceed 15% of its Tier 1 Capital, reinforcing that matched principal activity is not intended to create market risk or speculative exposure. Although the firm acts as principal, it performs an agency-like execution service, passing market risk immediately to clients and maintaining operational controls that ensure matching, segregation, and transparency.

As a result, Dealing as Matched Principal sits between pure agency dealing and full proprietary dealing, giving firms the ability to facilitate client trades efficiently while remaining within a tightly supervised risk framework.

Dealing in Investments as Principal

Dealing in Investments as Principal is a financial service in which a firm enters into transactions for its own account, taking full ownership of the assets or risks arising from those trades. Unlike agency or matched-principal dealing, a principal dealer buys and sells investments using its own capital, assumes market and credit risk, and may hold positions for strategic, market-making, or proprietary purposes.

Because these activities expose the firm directly to fluctuations in asset values and counterparty performance, the DFSA subjects principal dealers to significantly higher capital, systems-and-controls, and governance requirements.

Can DIFC firms service clients outside the centre, and in the greater UAE?

Yes. DIFC-licensed firms are permitted to service clients outside the DIFC, including clients located elsewhere in the UAE, provided that the financial service itself is carried on “in or from” the DIFC. This position was clarified under Dubai Law No. 5 of 2021, which expressly allows DIFC entities to offer and promote their products and services outside the physical boundaries of the Centre as long as the core activity, management, and operational substance remain within the DIFC. Firms may market, meet clients, conduct onboarding and relationship management across the UAE, but execution, booking, and regulated decision-making must occur from within the DIFC.

It is important to note that while DIFC authorisation allows cross-UAE marketing, certain activities—such as the marketing of funds or the distribution of onshore products—may require compliance with additional SCA onshore rules, particularly when targeting UAE mainland investors. In summary, DIFC firms can serve clients throughout the UAE as long as the regulated activity is anchored in the DIFC and they respect any additional sector-specific requirements imposed by other UAE regulators.

Can a DIFC-based brokerage firm engage in dealing in Crypto Assets?

Yes, a DFSA-regulated brokerages can deal in Crypto assets, provided that they are recognised Crypto Tokens. The DFSA has procedures for recognizing Crypto Tokens and maintains a list of such tokens. The current list of DFSA Recognised Crypto Tokens includes:

- Bitcoin (BTC).

- Ethereum (ETH).

- Litecoin (LTC).

- Toncoin (TON).

- XRP.

- ZetaChain (ZETA).

- EURC.

- USDC.

- Ripple (RLUSD).

What are the capital requirements for a Category 3A brokerage Firm?

The base capital requirement for a Category 3A Brokerage license is US$ 200,000, down from US$ 500,000 a few months ago.

The base capital requirement for a Category 2 Matched Principal license is US$ 500,000.

The base capital requirement for a Category 2 Principal Dealer license is US$ 2 million.

In many cases, firms also engage in the activity of Providing Custody, in which case the Base Capital will be at least US$ 500,000.

Actual capital resources required will depend on the nature, quantum of business and forecasted annual expenditure, as per the financial model of the proposed firm.

Capital waivers may be available to the DIFC branch of a regulated financial institution having its head office in a recognized regulatory jurisdiction.

The DFSA lists out multiple ways of calculating capital, and specifies capital requirements for a firm as the highest of the Base Capital, Risk-Based capital and Expense-Based Capital.

These figures are calculated using the financial models that we make for the Regulatory Business Plan during the application process and so are mostly unique to the company that applies for the license.

Calculation of capital is a detailed process and involves many factors. We recommend that you contact us for more details on the application processcontact us for more details on the application process and capital calculations.

What are the key staffing requirements in the DIFC?

As with other category firms, the DFSA expects that the firm be adequately staffed depending on the scale, scope and nature of the product portfolio that is proposed to be offered from the DIFC.

At a minimum, the DFSA would like to see the following appointments:

Board of Directors – a well-organized, diverse Board with Non-Executive and/or Independent Directors and robust governance policies. The Chair would have to be a non-executive Director.

Senior Executive Officer (SEO) – Senior finance professional with over 10-15 years of core experience, ordinarily resident in the UAE.

Finance Officer (FO) – Senior and suitably-qualified finance professional. In case of a group, the FO can be from the parent company and does not have to be resident in the UAE.

Risk Officer – Senior risk professional, can be from the parent entity in case of a group.

Compliance Officer (CO) - Senior compliance professional with over 10 years of experience, ordinarily resident in the UAE.

Money-Laundering Reporting Officer – Senior AML professional with over 10 years of experience, ordinarily resident in the UAE. This function can be combined with Compliance and one individual can carry out both responsibilities.

The Finance Officer, Compliance Officer and Money Laundering Reporting Officer roles can also be outsourced to a competent service provider, such as 10 Leaves.

Internal Auditor - Senior and suitably qualified internal audit professional. Usually outsourced to a professional firm.

External Auditor - Senior and suitably qualified external audit firm. The DFSA maintains a list of recognised auditors, and there are 16 such firms at present.

What is the process for licensing a brokerage firm in the DIFC?

The DIFC application process commences with formal introductions to the DIFC and the DFSA.

Following the introductory call, a detailed Regulatory Business Plan (RBP) is prepared, along with financial projections, for a quick review by the regulator.

The comments of the regulator are incorporated into the RBP, and a comprehensive application is compiled, comprising policies, processes and other related documentation. The KYC and associated forms of all key individuals are also prepared for submissions.

The formal application is then sent across to the DFSA, who reviews the pack over a period of 15-20 business days, and then accepts it. The detailed review process then commences, and this can take anywhere between 60 and 90 days to complete.

The regulator maintains communication with the applicant at all times during the review, reverting with an initial review 2 weeks into the application, and then follow-up reviews thereafter. The DFSA also meets with the SEO, FO and CO/MLRO designates, and conducts a detailed interview with them.

A key milestone is the issuance of an In-Principle Approval, or IPA, which is issued once the application is successful. The applicant then proceeds to satisfy the in-principle conditions, and this involves the setting up of a legal structure, opening a bank account, and depositing the share capital in the account. Other tasks include finalisation of auditors and obtaining professional indemnity insurance for the firm.

Once done, a final submission is made to the DFSA, following which the regulator issues the Financial Service Permissions and the process is then complete. The firm is now open for business.

What are the documents required for a DFSA brokerage license application?

The DFSA application is comprehensive and the application pack comprises detailed KYC forms and information, application forms, and policies and procedures including:

- Detailed Regulatory Business Plan.

- Detailed Financial model, including stress tested models.

- Risk Management Policy and framework.

- Compliance policies and procedures.

- AML policies and procedures.

- Business Continuity Plans.

- Process Flowcharts.

- Corporate Governance policies.

- Remuneration policies.

- Board Committees Terms of References.

- IT and Cyber Security Policies and procedures.

- Organisation and shareholding structure charts.

We assist with the preparation of all documentation as part of the authorisation process.

What are the associated costs?

Setting up a DFSA Regulated Firm involves the following costs:

Dubai Financial Services Authority (DFSA)

The DFSA is responsible for reviewing and approving all applications for financial services. Costs depend on the activities applied for, which puts the applicant in one of five categories.

Generally, there are two components of DFSA fees. One – an application processing fee, and the other, an annual licensing fee.

Application fee: US$ 25,000 for a Category 3A license application. The DFSA may charge an additional 100% fee for complex structures.

License fee: from US$ 25,000 for a Category 3A license. From 2025, an additional US$ 4,000 is charged as an annual fee per additional activity.

Registrar of Companies (DIFC ROC)

The ROC helps to set up the legal structure of the DIFC Regulated Firm. Shareholders can be individual, or corporate. There are many options available, such as ‘Private Company Limited by Shares’ and ‘Limited Liability Partnerships’. In case of Private Company Limited by Shares, the costs for setting up include:

Application for reserving a name (2 working days): US$ 800.

Application for Incorporation of a Private Company Limited by Shares (5 working days): US$ 8,000.

Commercial License on Incorporation (5 working days): US$ 12,000 (annual fee).

Data Protection

The data protection notification is part of the process of registering a new entity in the DIFC. The costs involved are as follows:

Registration - US$ 1,250.

Annual renewal – US$ 500.

Office spaces

Every entity registered in the DIFC is required to lease a physical office. You can choose from the Gate and surrounding buildings, or other buildings within the DIFC, such as Emirates Financial Towers, Central Park, Park Avenue, Burj Daman and Currency House.

Prices vary, depending on the space availed and the building. Here is an indication of the prevailing rates:

DIFC Business Centre – from a one-desk office at US$ 30,000.

DIFC Fitted Offices – from US$ 55 per square foot.

Other buildings – from US$ 50,000 per annum.

Visas

Establishment Card Application – US$ 630.

PSA Deposit – US$ 682.

Visas (per visa) – from US$ 1,500.

PSA Deposit (per visa) – US$ 682.

Our Services

How can we at 10 Leaves assist you?

We provide turnkey services for DIFC Brokerage Licenses. From initial consultations to assistance in authorisations, to assistance in preparation of the legal documentation, 10 Leaves helps you navigate the DFSA Rulebook and submit an application that is comprehensive, complete and compliant.

Our services include assistance in:

Pre-Licensing

- Reviewing the business model and advice on the applicable regulatory framework;

- Preparation of the Regulatory Business Plan and comprehensive financial projections;

- Preparation of all policies, processes and manuals required;

- Provision of Outsourced services, including outsourced Compliance Officer, outsourced Finance Officer and outsourced Risk Officer services;

- Assistance in recruitment of senior management;

- Provision of well-qualified and experienced Non-Executive Directors;

- Finalising the legal structure, including holding company setup and customisation of Memorandums; and

- Finalisation of leased space, bank account opening and obtaining Financial Services Permissions.

Post-Licensing

- Compliance, Finance and Risk outsourced and support services.

- VAT and Corporate Tax services.

- Secretarial services.

- Variation of Permissions.

- Compliance remedial measures.

- Compliance audits.

- Training.

- Senior-level recruitment services.

Our solution focuses on comprehensive training for Directors, Senior Executive Officers, Finance Officers, and Compliance Officers. We equip them with the knowledge and skills needed to successfully clear interviews conducted by the DFSA during the authorisation process and for ongoing compliance.

We also assist such teams with corporate and commercial documentation through our legal consultancy - 10 Leaves Legability. We assist in the drafting of:

- Founder agreements.

- Shareholder agreements.

- Investor agreements.

- Share vesting/ESOP plans.

- Client/Supplier/Distributor agreements.

- Employment agreements.

We also provide services in Luxembourg, Saudi Arabia, India and Mauritius.

Get in touch today! to know more about the DIFC Category 3A Brokerage License.

CONTACT

CONTACT